Digital

Cash

What is Digital Cash?

Digital Cash acts much like real cash, except that it’s not

on paper. Money in your bank account is

converted to a digital code. This digital

code may then be stored on a microchip, a pocket card (like a smart card), or

on the hard drive of your computer.

The concept of privacy is the driving force behind digital

cash. The user of digital cash is

assured an anonymous transaction by any vendor who accepts it. Your special bank account code can be used

over the internet or at any participating merchant to purchase an item. Everybody involved in the transaction, from

the bank to the user to the vendor, agree to recognize the worth of the

transaction, and thus create this new form or exchange.

How does Digital Cash work?

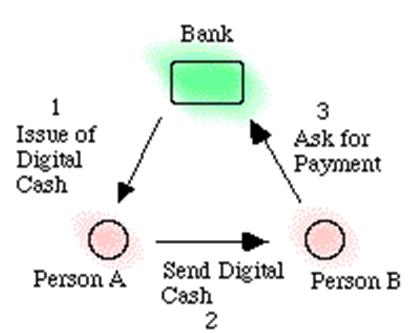

This example shows how digital cash might work

through a banking institution. The bank

creates a digital bank note by signing a message which specifies the serial

number (with a primary or public key) and value of the note, and sends it to

Person A. Person A, as he withdraws it, uses Chaum's technique (A Cryptography

technique) to alter the serial number so that the bank will not recognize the

note as being from this withdrawal. This note is now returned to the bank with

the new serial number. The bank now has

a note with a new serial number. Person

A then pays Person B electronically by sending the bank note to him. Person B

checks the note's validity by decrypting using the bank's public key to check

its signature (new serial number validity). Person B then sends the note to the

bank, which checks the serial number to confirm that this bank note hasn't been

spent before. The serial number is now different from that in Person A’s

withdrawal, thereby pre- venting the bank from linking the two transactions.

The enabling bank merely checks the new serialized key account for the amount

of the transaction and transfers the money by sending out a depository

notice. Person B using the same

encrypting technique returns the depository notice with the new serialize

account. The enabling bank does not know

who the merchant is only that money is available for payment. In some respects, this is a debit card

transaction with no information other than the amount of the transaction. All initial depositor information is in the

primary key account not the password account.

Special software to enable these dual track procedures was

developed by Digicash. However this

venture was not successful, nor was it successful for its successor

corporation, CyberCash, Inc.

What is the Future Vision for Digital

Cash?

The future vision is that Digital Cash be a true Internet

e-commerce structure with virtual banks created solely for the purpose of

transactions clearing. The unit of money

envisioned would not be limited to a cash equivalent of a unit of money from a

specific country, but instead would be some Electronic Digital Equivalent Unit

(EDEU). At the time the initial notes

would be issued from the enabling bank the EDEU, would be set. Thereafter all transactions would be in the

EDEU.

There is some resistance to this from governments. In this system, an entity other than a

governmental unit would in effect be issuing money. Governments are concerned about its possible

effects on the stability of financial markets, its effects on monetary policy,

its effects on consumer protections (such as our FDIC, and FSLIC programs), and

possible criminal activity effects.

Most experts believe that the use of the internet for

electronic transactions and the use of digital cash will rapidly over the next

ten to twenty years, but that a fully integrated international unit of currency

approach will not happen any time soon.

In the near future it seems that financial transactions will continue in

the same financial market clearinghouse that is in use for current e-commerce

systems.

Resources on the Web:

Class research website, has good background information for issues involved, includes other electronic payment systems also

http://www.sims.berkeley.edu/courses/is204/f97/GroupE/

Digital Cash White Paper:

http://www.isoc.org/HMP/PAPER/136/html/paper.html

“Possible Economic Consequences of Digital Cash”

http://www.firstmonday.dk/issues/issue2/digital_cash/#overview

“Cashless Society or Digital Cash?”

http://www.sfasu.edu/finance/FINCASH.HTM

Book on Ecommerce Topics: Electronic Payment Systems for E-Commerce by Donal O’Mahony, Michael Pierce, and Hitesh Tewari

Good websites for Topics and Links to other sites:

Electronic Money or E-Money or Digital Cash

http://www.ex.ac.uk/~RDavies/arian/emoney.html

http://www.ecommerce1.com/digital_cash.htm

Yahoos Website of Companies

Interent site for Ecommerce sources

http://www.ecommerce1.com/digital_cash.htm

A discussion site for Network Payment Mechanisms

http://ganges.cs.tcd.ie/mepeirce/Project/mlists.html

Feds concern about digital cash

http://www.wired.com/news/politics/0,1283,38955,00.html

Web Page explaining the mathematics behind digital cash cryptography

http://www.aci.net/kalliste/cryptnum.htm

Warns about the proliferation of bad consequences from digital cash

http://www.privacyexchange.org/iss/confpro/cfpuntraceable.html

E-GOLD References

requested by Professor:

http://www.wired.com/news/ebiz/0,1272,44967,00.html

/